2021:3 Shorts going through the roof, 6% US vaccination, VC funded public companies, Starbucks drive tru, Fundsmith letter, is covid going to change habits?, quantum computing and earnings season

An eclectic mix of things passed by my desk this week. Lots of annual letters are coming out. As expected: 2020 performance differs widely - which is not unusual after a year like 2020 - so interesting to see how everybody comments on the year. In the meantime: equity markets in general are up with emerging markets (particularly Asia) in the lead.

Enjoy and feel free to reach out!

(And again a quick housekeeping reminder: no investment advice to be found here - just gathering some things that passed by my desk.)

I had fun reading the yearly letter of Bronte Capital. If I understand correctly (from podcasts and so on) - their long book is fairly large cap high quality and their short book exists out of lots of smaller positions (accounting fraud, promoted stocks, CEOs with fraud background,…). That last bit is obviously struggling in this environment:

Historically the biggest driver of our short book – and the driver that has worked best for us – is shorting stocks aggressively promoted to retail investors. We seek to find the most cynical and self-serving promoters who promote fads, frauds and failures to retail investors. But “sold to naïve investors” is a basic tell.

If your main schtick is finding the dumbest retail investors and shorting whatever has been sold to them then you have done poorly. This sort of bullish investor may have the intelligence of their bovine counterparts, but a herd of them can gore you.

Related to that he talks p/sales multiples, SPACs and ESG flows. Basically “flows” that are currently hard to bet against (i.e. you could be right in the longer term but you also could get crushed by flows in the meantime).

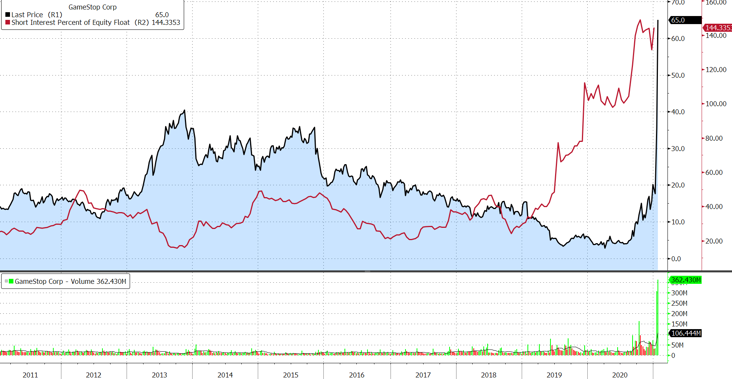

The recent story from Gamestop probably adds to this:

The short interest of GME was really through the roof btw:

Last week I shared a tweet with some highly shorted names — the performance of these kind of names is captured by the GS Most Short Index - which has outperformed in a big way the last couple of weeks:

The performance of non-profitable tech names and IPO’s can be added here as a sentiment check in certain parts of the market.

Bronte also spends some extra words on Pinduoduo:

Pinduoduo has none of the features that we associate with sustainable multi-level marketing schemes (and we think we have some expertise). Moreover, large hierarchical organizations in China (including such schemes) either wind up being heavily answerable to the Communist Party or dismantled as a threat to the Party.

The accounts at Pinduoduo are “interesting” in the same sense as the purported Chinese proverb. And Pinduoduo has never generated cash, whereas MLMs normally have negative working capital and are highly cash generative in the growth phase.

But, whatever, Pinduoduo is fast growing and it is in China.

For those not familiar with the company (per Wikipedia):

Pinduoduo Inc. (Chinese: 拼多多; Pinyin: Pīn duōduō) is the largest agriculture-focused technology platform in China, serving 731 million active buyers as of September 2020.[2][3][4] It has created a platform that connects farmers and distributors with consumers directly through its interactive shopping experience. In 2019, nearly 600,000 merchants sold farm produce through Pinduoduo. That translated to some 12 million farmers who supplied their fruits and vegetables to the merchants. In August, Pinduoduo pledged to sell $145 billion worth of farm produce annually by 2025.

Bloomberg does a good job of tracking global vaccinations. I was surprised by the 6% in the US. They do on average about 1 mln. doses per day:

Guess Belgium (were I live) is not last — but no harm in moving a bit up the ladder I guess:

In the meantime - I feel the progress of Johnson&Johnson vaccine didn’t get a lot of press attention. It could be approved for EUA within two weeks according to Fauci:

“I would be surprised if it was any more than two weeks from now that the data will be analyzed and decisions would be made” about the vaccine being developed by Johnson & Johnson, Fauci said during an appearance on Rachel Maddow’s MSNBC show.

“We’ll look at the data and determine if it’s ready to be given to the public,” Fauci said, “so they can go to the FDA to ask if they can get an emergency-use authorization.”

Btw: EU and US have quite different vaccine portfolios (from the FT). The US has both the mRNA vaccine from Pfizer and Moderna. A Johnson&Johnson approval could be benificial for the EU to increase the supply:

Nice overview of VC-Funded US companies that went public dec 2019 - present:

Fundsmith 2020 letter was out last week. They bought some new companies last year:

In the case of Nike we felt that few companies were as well adapted to digital distribution of its products which has become de rigeur as a result of the COVID induced restrictions.

Whilst it is easy to see the challenge to the lockdowns for Starbucks’s urban outlets which partly rely on seating and coffee collected on the way to the office, this is far from their only format. The sometimes spectacular queues and resulting traffic jams at Starbucks drivethrough outlets both illustrate another format and testify to the continued loyalty to the brand as does the rise in loyalty club members in 2020. During this period Starbucks’s main competitor in its second largest market — Luckin Coffee in China — was exposed as a fraud in yet another illustration of the rule that it is only when the tide goes out that you find out who has been swimming naked.

After the COVID lockdowns we also purchased a stake in LVMH — the world’s leading designer and luxury goods business. Although we had some exposure to luxury goods through our cosmetics and drinks companies, we had no exposure to designer apparel and jewellery which LVMH brings.

As always they give an insight on the portfolio characteristics - fundamentally and cost wise (which is an important recurring element in their publications - especially with regard to “hidden” fees such as transaction costs). And they talk intangibles.

Be sure to also check out the recordings of their annual meetings. They are a fun watch.

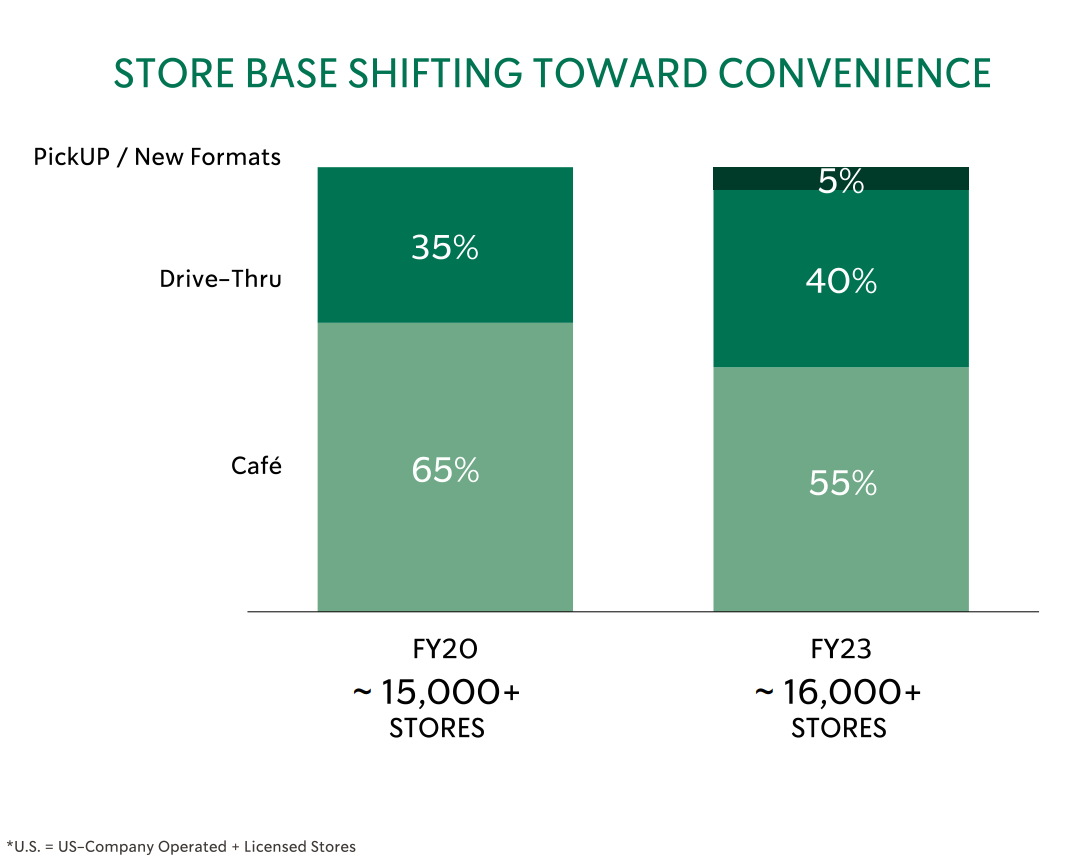

Starbucks drive-tru was also mentioned by Sean Stannard-Stockton from Ensemble Capital in a recent podcast with Bill Brewster. With regard to store base (café, drive-true and pickup) from their 2020 investor day:

They don’t have one in Belgium I believe - but there are two coming to the Netherlands. It feels “American” to me - but I guess it can work here:

About the pandemic changing some trends/habits: even though Fundsmith is no macro/trend investor (but in the end everybody is it to a certain extent I guess):

One of the conclusions that you might draw from the economic effects of pandemics is that they do not so much cause new trends but rather they accelerate some existing trends.

Obviously, I do not know, and fortunately my predictive capability is not the basis of our investment strategy. However, there are some clear signs that existing trends have been accelerated by COVID. For example:

e-commerce

online working from remote locations using the cloud or distributed computing

home cooking and food delivery

online schooling and medicine

social media and communications

pets - which have become more important in isolation and when their owners are more at home

automation and AI

Dennis Lynch talked about this on a Nov/20 podcast with MIB:

Generally, in a the time of crisis, you’re going to see a more likelihood of faster adaption or people sort of looking more at the world from a blank sheet of paper standpoint and more likely to do things that are different and change their behavior.

He also talked to GS recently:

I feel he talks on a pretty down to earth tone and he mentions the luck and team aspect in both conversations.

You also have a piece from Gavin Baker about suits and business travel:

Suits are cyclical. Almost all offices go casual late in the cycle. Then the economy rolls over and a few months into the recession, someone shows up at the office wearing a suit because they are worried about their job. The next day everyone is wearing a suit.

Business travel will be the same. Every business will try to avoid travel and stay on Zoom. But then one company, struggling with sales, will send their sales representatives on the road and conversions will increase. The next quarter all of their competitors will be on the road. The same will go for conferences, for diligence, for deals, for executive retreats, for everything.

Travel and office (real estate) is probably debated most heavily: Brian Chesky (CEO AirBnB) said the following a few weeks ago:

If you look at the majority of profits of hotels and airlines: it was business travel.

What is gonna happen - instead of people only travelling to top 50 cities in the world, crowding in hotel districts - many will now travel by car and they are gonna travel to thousands of smaller communities. And many communities are going to be smaller cities or rural areas. Farms stays are huge now.

Before Times Square - people want to first see their family and friends. Mass travel is going to be replaced by meaningful travel.

Guess he is also talking his own book a bit ;)

I also liked the view - I believe from Siegel in a Behind the Markets podcast - where he basically says that because this situation (lockdown etc.) really took some months - some habits might have changed for the longer term.

Was sniffing around on the Counterpoint Global (Morgan Stanley) website and bumped into a piece around quantum computing.

The notion that Moore’s Law, the idea that classical computing capability doubles every two years, is dead has gained traction in recent years. Quantum computing offers a possible path to continue the improvement in computing. While still nascent, quantum computing has the potential to improve much faster than the rate suggested by Moore’s Law. In fact, quantum computing is said to follow Neven’s Law, which states, “Quantum computing is experiencing doubly exponential growth relative to conventional computing.” If Neven’s Law proves true, we can expect to see huge advances in quantum computing over the next decade. Quantum computing offers the potential to improve our lives by enabling everything from better renewable energy technologies to new drugs to cure complex diseases. Quantum computing could become a foundational technology in the decades ahead.

Quantum computing is also on the Ark investigation list (from a 2020 Bloomberg interview).

Quarterly numbers are rolling in - not going to comment as such of course on specifics. But saw some things passing by:

check out the Netflix letter - highly readable (and given lots of people watch Netflix - they get a lot of what they are writing about) - they highlighted themselves the piece on cash-flow

We believe we are very close to being sustainably FCF positive. For the full year 2021, we currently anticipate free cash flow will be around break even (vs. our prior expectation for -$1 billion to break even). Combined with our $8.2 billion cash balance and our $750m undrawn credit facility, we believe we no longer have a need to raise external financing for our day-to-day operations. Our 5.375% February 1, 2021 bonds mature in Q1. We plan on repaying the bond at maturity out of cash on hand, as we are currently well above our minimum cash needs.

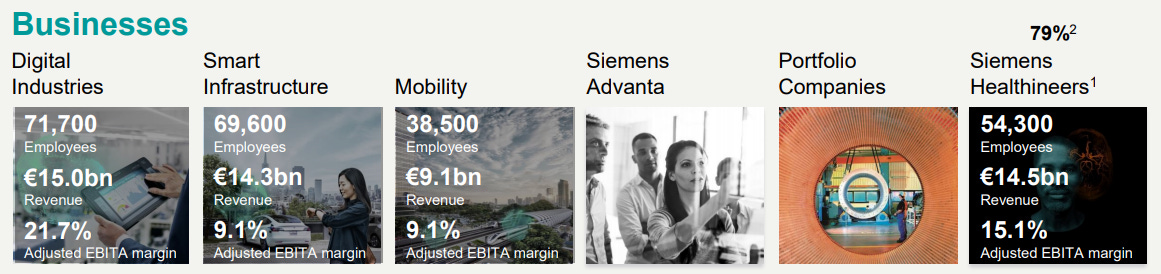

Siemens surprised markets in Digital industries and Smart Infrastructure - which makes up the biggest part of their business:

IBM investors didn’t enjoy the numbers that much. I do remember the words from Chanos on a recent Real Vision interview:

Fast forward to a year ago - and when IBM decided to buy Red Hat for $34 billion in debt to jumpstart their cloud business, we decided to take another look.

What we saw was that the operating morass that we saw back in 2014-2015 had gotten far worse, that now, the revenue declines were solidly mid-single digits year-over-year. They had cut costs as far as they could cut. The drops in revenues were now dropping to the operating line.

Even more so - the company was getting more and more aggressive with how it booked things like tax credits and one-time items to make up the shortfall.

Enjoy!