2020:6 platforms, future winners, semiconductors and ARK

As an intro - bumped into this opening paragraph from Liberty’s substack. I do like it and tend to agree with the Amazon approach: do lots of small experiments, then put more time and energy behind those that work.

If you’ve been a lurker on Twitter or forums or have wanted to start a blog or a newsletter but haven’t because you think you’ve got nothing to contribute and you wouldn’t be good at it anyway, the way to get out of that unproductive loop is to just punch through and do it (Arnold voice: dooo iiiit!).

If you don’t, you can be 100% certain nothing will happen. If you do, I can’t promise success, but there’s a non-zero chance that you’ll find out it was a good idea, and that all those other people you’ve been reading aren’t special, they just gave it a try and have been learning from the experience ever since.

Throw your hat in the ring, you can always take it out if it’s really not for you. Be like Amazon, do lots of small experiments, then put more time and energy behind those that work, and drop those that don’t (also remember Bezos’s two-way doors vs one-way doors).

Don’t sit around waiting to know in advance that something will be 100% perfect before acting, that never happens.

The Amazon approach for me probably means: don’t wait until you have a special topic or so - just write down your thoughts, enjoy and learn something on the way there. We will see where it ends.

Mostly Borrowed Ideas pointed me to a nice post from Sparkline Capital. “Platform” is a magical word these days, and I guess rightfully so. What Sparkline Capital did:

We will compare the 10-Ks to two articles from platform experts Eisennman, Parker and Van Alstyne (2006 , 2007). We use both articles as one deals with transaction platforms and the other innovation platforms. We also mask company names so that our algorithm focuses only on the general features of the platform business model itself.

(Disclaimer: no ML expert here)

In particular, I liked some visualisations. First: how a company like Amazon moved up the platform scale:

And two, how most stock returns from these companies came from sales growth (and only recently, you also see a P/E expansion):

According to the author, platforms have been most successful disrupting industries with inefficient gatekeepers, high fragmentation and untapped supply. And finally a really important element to understand the current market position/share of some companies:

The endgame of positive feedback is monopoly. It is not efficient to have liquidity fragmented across hundreds of stock exchanges, social networks, or mobile operating systems. Ultimately, positive feedback will tip the market toward one or two dominant players.

And the conclusion:

Platforms have become a dominant economic force. Their ascent has disrupted dozens of industries, created massive concentrations of power, and transformed many aspects of society.

However, investors have been slow to recognize the power of the platform business model. Platforms have handily outperformed the stock market for over a decade. We believe this is due to the complexity of cleanly identifying platform companies and valuing intangible network effects.

Network effects lead to positive feedback and monopoly, which disrupt traditional investment approaches. Given their increasing importance, investors would be well served to devote resources to deeply understanding the platform business model.

Rereading previous Nike’s earnings call and especially the remarks with regard to digital:

This is the first quarter since the start of the pandemic where our retail was essentially opened, and as more consumers return to our stores, we saw impressive conversion in-store, even as our digital business accelerated even further. Our store traffic and sales are improving quarter-over-quarter and we're also seeing consumers increasingly self-identify as a member during checkout, or as we call it, a linked transaction, which is leading to even more engagement on our apps and an elevated O2O journey.

Our new store in Guangzhou is a data-powered store concept that curates a one-to-one personalized shopping journey. We're already seeing member checkout in our Guangzhou store significantly outpace the rest of the fleet.

I’m also digesting a piece of Gavin Baker from a while ago:

I believe the biggest long term beneficiaries of Covid will prove to be category leading brick and mortar retailers. By this I simply mean brick and mortar retailers who have dominant share in a category — whether it be home improvement, general merchandise, electronics or any other retail category. Their destiny has likely changed forever. Many of the perceived Covid winners such as e-commerce, videogame and streaming media companies have simply been pulled a few years forward into a future that was inevitable. Their destiny did not change. The future for those businesses simply accelerated whereas the future for category leading “brick and mortar” retailers has changed dramatically as a result of Covid

Not totally related - but I also saved the words from the CEO of Starbucks (from an FT article):

“People will be back in Starbucks stores at a rate far beyond what they were pre-pandemic,” he said in an interview on the eve of a biennial investor day.

“Smaller speciality chains, the mom and pop coffee shops . . . don’t have the balance sheets that Starbucks has,” said RJ Hottovy, consumer equity strategist at Morningstar.

Larger groups have also struggled: Caffè Nero, the UK’s third-biggest chain, has been forced into a financial restructuring, while Pret A Manger has axed 3,000 people. “There’s going to be a lot fewer coffee shops,” Mr Hottovy noted. “Starbucks stands to benefit from that.”

“You can have connections digitally but . . . you want to have those in-person connections,” he said. “That is just an inherent part of being human.”

Also noted this:

Starbucks announced last month that wages for baristas and other employees in the US would rise by at least 10 per cent. The move positions Starbucks for the prospect of higher minimum wages across the country, but Mr Johnson described it as “one of the most significant investments” the company will make this decade.

In the end, I feel everybody tries to figure out who comes out stronger at the other end of the corona tunnel. Some winners - like Zoom for example - are obvious winners during this pandemic. Who wins the period after this is less clear. My two cents is we could see a lot of “normal” life/business practices again, especially in the beginning.

Semiconductors remain a popular discussing topic these days. The combo of:

overall demand / use of chips tailwind

multiple players in the value chain that realize a nice profit

changing dynamics in the industry

make it a nice hunting/debating ground. Although I do agree with these arguments, I also see:

an industry that is highly technical - even if you do lots of work on it and/or would apply the 80/20 rule (to not get after every detail) - the production process/details/dynamics are not easy to understand imho

changing dynamics doesn’t necessarily makes it easier to cut through the noise or predict the direction of the industry

and: even though business model comes before valuation, lots of attention has put some companies at not so cheap valuations. One can argue that some have reduced cyclicality, but still. Current “winners” like ASML and Nvidia trade around 50x earnings.

In terms of overall industry direction, I liked the article of Mule “Tech monopolies go vertical”:

The push and tug will be violent, but clearly, the ball is in the large software companies’ court. They are right now the leading edge of all innovation on the internet, and now many hyperscalers will be some of the first in line at leading-edge fabs. The void left behind in Intel’s wake is massive, and everyone realizes that they can benefit from their “death” by bringing their own silicon and creating an end to end platform that cannot be replicated.

Software ate the world and hardware has been struggling to keep up recently. Now the largest software companies are slowly becoming hardware companies and pursuing an integrated strategy that only can be achieved at the largest scale possible and with barriers of entry that are quickly expanding in addition to their well-known network or aggregation effects. The walls are slowly rising, the moats slowly widening, and as we are on the cusp of a new hardware renaissance, the decisions the hyperscalers make now are going to have a long-lasting competitive shadow. Stay tuned.

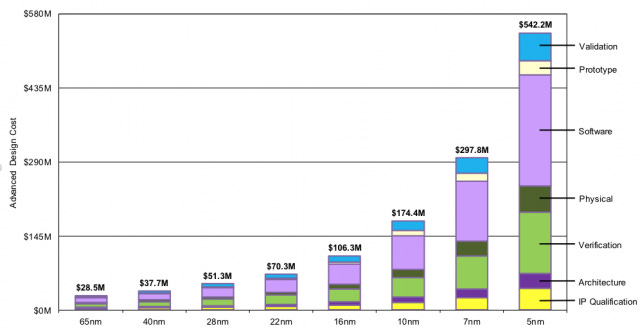

He also points out the design cost of a chip. The cash on the balanced sheet of the tech giants seems to have found a something to invest in I guess:

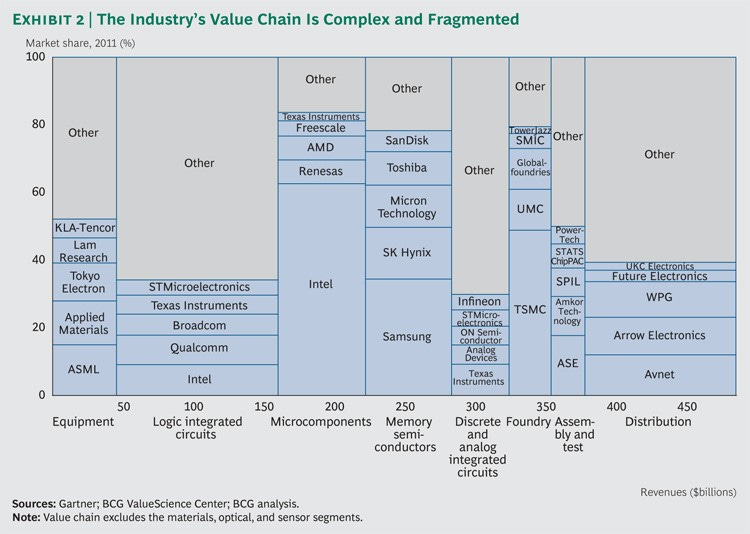

I found this 2011 industry picture from BCG (no Nvidia to be seen):

You have to admit they were on to something:

Although we do not expect the integrated model to disappear, it is coming under sustained attack from the fast-growing “fabless foundry” approach, which breaks down the design and manufacturing process and involves different companies concentrating on distinct functions or intellectual property blocks. Fabless designers (such as Avago Technologies, Broadcom, Marvell, MediaTek, Qualcomm, and Xilinx) and high-efficiency, low-cost foundries (such as Globalfoundries, Taiwan Semiconductor Manufacturing Company [TSMC], and United Microelectronics Corporation [UMC]) have staked out large and growing positions, attempting to flank their vertically-integrated competitors (such as Intel, Samsung, and Toshiba). The trend toward deconstruction is most pronounced in the digital segment, where product life cycles are short, capital requirements are high, and scale matters. Vertically integrated manufacturers remain especially strong in the analog segment, where product life cycles are significantly longer and proprietary manufacturing processes have been developed.

The WSJ/Bloomberg ran a nice summarizing article. As mentioned in the beginning - the market is discounting the future and changing environments. Currently, Intel still has leading marketshare in servermarket and ARM-based central processors are a minority:

I’m pretty late to the ARK party. Although looking at AuM evolution - the big inflows only came after the initial corona sell-off and even more so the last couple of months.

They are further out on the “innovation” scale than our average portfolios (which I don’t discuss here) - but they share lots of their research - so lots of interesting datapoints can be found on their website as “a challenge”.

Be it traditional farma (genomics), banks (Square, Paypal), transportation (EV),… there is something for everybody I believe. Look for example at their estimation of the cost-per-ton-mile by mode:

Do you need to believe this? Nope for sure not. But why not think about it or ask around to see what other people think about it. And how feasible and/or nearby this could be. If you own a train company - which has been an excellent investment the last couple of years - no harm in trying to find out the 3 cents of autonomous EV trucking is realistic.

To wrap-up: Value Hive did a nice talk with Brett Winton. They also talk about the research process - where they combine top-down theme research and bottom up 5 year valuations:

Although everybody fights their behavioral biases, I do realize the extreme outperformance of the strategies might make the process look more useful (ie with bad returns lots of people would think like: “mm yeah sounds fancy but don’t know it would work in practice…mm look at returns…mm”). Still: I feel the attempt to bring in more external opinies (online, crowdsourced, professors,…) is always a good idea. The key is still you do need a good aggregator (in terms of research and portfolio management) to put all these bits and pieces together.

Lastly, Bloomberg did an interview with Cathie Wood last week. Genomics seems to be her favorite current theme, and quantum computing might be on there investigation list:

Enjoy! And feel free to reach out!