2021:2 Failed French takeover, US resto, semi (again), non-profitable tech winning and oil majors renewable investments

Second write-up for 2021.

Equity markets show a positive return year to date. EM (Asia) is winning regionally. I feel however lots of things going on underneath the small plus (as always I guess). Semi newsflow keeps coming - with TSMC capex pushing a range of semi capital equipment names higher. In the meantime - big tech is flat since the summer (also: the value trade - banks and oil - is up since US elections). And we had a failed takeover bid for a French company.

Enjoy!

Last week Wednesday, the Canadian Couche-Tard announced a EUR 20/share takeover offer for the French Carrefour. On Friday however, it was abandoned - citing French government resistance as a hurdle.

Remember Danone in 2005? Pepsi appointed investment bankers to look at a potential tie-up. You could wonder whether France has to update their list of “key strategic” companies (guess yoghurt or food retail shouldn’t be in there right?).

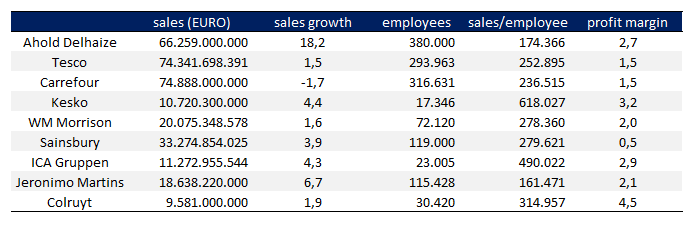

If we look at the MSCI Europe - there are about nine quoted food retailers. In terms of marketcap: Ahold and Tesco represent 60% - Carrefour is next with about 10%. Was looking at some numbers:

The general thought is that food retail is high volume at low margin. And also: it is not easy to grow sales. Both locally in satured developed markets and also international expansion has proven challenging.

In 2016, Tesco ditched their global ambitions:

Walmart acquired the UK-based Asda for $ 10.8 billion in 1999 - it was recently sold for $ 8.8 billion (also influenced by regulatory blocked merger with Sainsbury):

There is a 2012 HBR-article talking about the dangers of international expansion of food retailers:

It’s tough for retailers to enter overseas or foreign markets by acquiring local players. In developed markets, few retailers want to sell. Moreover, foreign entrants struggle to bring offerings to developed countries that shoppers perceive as new, different, and valuable.

The process of building a network of stores to a profitable scale takes a long time and entails large investments that may not pay off for decades. Walmart broke even in China in 2010, after 15 long years of investment.

These “country killers” understand local preferences and tailor offerings to local consumers’ needs.

Btw, I also like this comment on the grocery suppliers (think Nestlé, Unilever,…) - you can see why they have less trouble expanding worldwide (although paprika flavoured chips and sparkling Ice-Tea is a hard find when travelling):

unlike grocery suppliers, which can profitably cater to one consumer segment across a country, mass-market retailers must compete for every consumer in the economically diverse trading area of each store. They don’t enjoy the luxury of selecting slices of consumers; they have to make every store profitable despite the mix of clientele in the surrounding area.

Of course - not saying everything is bad within food retail: Colruyt is actually a good efficient operator, AholdDelhaize worked out OK and they hold bol.com and a Walmart is a high quality retailer that is aware of the e-commerce evolution.

As a final note: for the coming years - I’m curious what % of food & beverage sales will go towards a collect&go or home delivery formula. Different sources cite quite different numbers but I guess the global pandemic might have shifted some shopping habits:

Totally different industry but somehow related: end 2019 the FT published a good piece “Why the global telecoms dream turned sour”. In the end also telecoms tried to grab faster growth in emerging markets - but in the end these investments yielded little return:

Yet the industry’s dream has long soured, unable to build truly global brands like the leading tech groups and media providers that piggybacked on the industry’s infrastructure. The sector’s biggest names, which had built subscriber bases equivalent to the populations of large countries — by 2014, Vodafone had 434m customers — have started to retreat from their far-flung empires. Seen initially as engines for growth, much of the telecoms colonialism yielded little return on investment and, for the likes of Telia, hefty fines related to corruption.

Interesting visualisation about US restaurant industry (although delivery split-up would have been a nice addition anno 2020!):

Again semi news this week with a new CEO for Intel. Jon Masters has a good summary:

Thus, we are entering a decade in which the market is ripe for cloud players to dominate the technical direction (which we are already seeing), and I expect this to accelerate rapidly.

So what would I do if I were Pat? I would think carefully about all of the above. The next decade isn’t going to be “x86 vs Arm”, or “x86 vs Arm vs RISC-V”. It isn’t going to be some motherboard with a chip and a bunch of PCIe slots you plug whatever adapter widget into. Nobody cares any more. Compute is a boring commodity. It’s something I can license and build for myself if I’m large enough (and many are). The future is about carefully marrying all of the different possibilities together into a whole that includes both compute, as well as acceleration, and leveraging hw/sw co-design.

It seems most people praise Intel for picking an engineer. It might also give the company a few weeks of positive honeymoon news.

Daniel Loeb (Third Point) - who is an activist on Intel - posted a video of Pat Gelsinger when he was still at VMware (which I still have to watch):

Mule did a good summary of the TSMC earnings: headline takeaways:

capex $25-28 billion (vs $19 billion in 2019) - because of demand and higher complexity processes

seasonality being lower (as somebody pointed out on Twitter - already playing out for multiple years) - because of multiple customers and multiple end markets

TSMC is diversified across nodes and end clients / markets:

And to finish: Odd Lots did another semi podcast. They talk about semi of course - but also been thinking about a comment that China wants the world to buy from them - but in the meantime they also try to build for themselves (so they don’t need to buy from the world anymore). Well: to have both ways is going to be though.

And there is this wording on yields:

FYI: “Wafer fabrication yield or fab yield - this is defined as the ratio of the total number of wafers that come out of the fab (after the end of all the individual processes, including measurement) to the total number of wafers that were started in the fab.”

Although I can’t see which companies are in the index (so not 100% sure which factors are at play exactly) - I find the return graph below a fascinating one. Red is “big tech” and blue is “non-profitable tech”. Basically big tech - think Microsoft, Amazon,… - is dead money since the summer. In the meantime Microsoft is trading at 28x 2020 P/E versus S&P 500 at 20x P/E.

And of course - reality is always complicated: GAAP EPS (i.e. profit) is never painting the whole picture, the companies are investing through their P&L, there are intangibles and these are often new high growth technologies. Still it feels for example IPO pops are pretty big. The Renaissance IPO index is up over 100% over a 1 year period - the correlation since last summer between IPO and non-profitable tech is no coincidence of course:

Some historical perspective on IPO’s:

Some enterprise software companies are trading at quite high sales multiples - some are definitely part of the no-profit software index above. And some are surprisingly big already in terms of marketcap.

(Not sure Shopify should be in this list - but that wouldn’t change the overall picture.)

In terms of sentiment not related to tech: some heavily shorted names have enjoyed outsized returns (note these names aren not always the biggest companies so not driving overall equity market returns):

A few weeks ago I was looking at wind energy ecosystem. Last Friday I was browsing through installed / planned wind (and renewables in general) of European utilities and energy companies.

I came across this 2019 paper which actually sums up nice the M&A capital allocation decisions of the major oil majors.

In a next post I might put operational cash flow and capex of the oil majors and utility players next to each other. Both are making big efforts to move towards more renewables. But the dedication differs in terms of capex and end goals. I feel in terms of installed capacity and capex - utilities were winning the last couple of years. Oil majors however have a considerable amount of operational cash flow to spend and playing catch-up (also buying into windfarms for example - instead of developing from scratch).

In the long term: both oil majors and utilities will overlap in terms of renewable energy generation assets. Differences might remain i.e. oil majors clearly will still have oil and mostly don’t have grid assets (i.e. most utilities have somewhere a local grid in their portfolios).

Some history to finish the week: I liked this video with regard to the name of the company Orsted:

Hans Christian Ørsted; often rendered Oersted in English; 14 August 1777 – 9 March 1851) was a Danish physicist and chemist who discovered that electric currents create magnetic fields, which was the first connection found between electricity and magnetism. Oersted's law and the oersted (Oe) are named after him.

Enjoy!