2021:5 doing the hard 1st principles work, RISC-V, innovation, EV battery value chain, L'oreal, Tencent and TI analog engineers

During the past week - I listened to quite some podcasts. Be sure to check out the ones below. And say hello to Jonathan on Twitter for his 189th birthday (he pops up somewhere in the middle of the substack).

Enjoy!

Odd Lots keeps publishing some high quality podcasts - I would like to highlight three recent ones I listened to this week:

Ark’s Head of Research Brett Winton. Whether you like or dislike (certain elements of) them: there is something to learn here. First of all how they organise themselves namely by technology and not by sector/industry. Secondly their openness is a key part of their research process:

The analyst need to be able to discuss what they believe - both in written form and orally - so that they uncover their own weaknesses. Having to publish makes you a much better and more diligent modeler. If you dig into the underpinnings of models that aren’t published: they are always a mess - they are always poorly documented - there are always things where people just say “aah I picked that because I wanted to”. Whereas, both the auditing process we have to go true in order to get something published and the process along the way where you distill it to its most elemental understandable form - forces us to be better at our job. And once you publish you get better again - because you get this great feedback loop of people telling you what you got wrong.

The hard part is not to let people share their work - but to do the hard first principles work in the first place. There are a lot of people who are not used to being intellectually ambitious.

You get more out of the information ecosystem by providing information into it.

Benn Eifert on (the Gamestop) boom in (options) retail trading. He explains the gamma squeeze but also an important point in “trading”: never trade against a strong hand. With Tesla as an example (i.e. especially the original owners of the stock were/are die hard believers).

Chris Lattner in the the semiconductor series talking about RISC-V. I guess - the more you try to understand about semi - the less you know ;) There was a recent discussion about RISC-V on CES 2021 that might help here:

RISC-V also pops up in the Ark 2021 Big Ideas presentation.

With regard to “innovation”: people - like Brett Winton of Ark - often talk about some laws, theories and curves. The main goal is to provide some kind of framework and/or thinking pattern about innovations and new technologies:

General-purpose technologies (GPTs) are technologies that can affect an entire economy (usually at a national or global level). GPTs have the potential to drastically alter societies through their impact on pre-existing economic and social structures.

As you can see - there is not always consensus whether something qualifies as a GPT. The table contains historical examples - so imagine the debate about current or future GPT.

By now - everybody knows Moore’s Law I guess. But you also have Wright’s Law:

It states that for every cumulative doubling of units produced, costs will fall by a constant percentage.

And example are EV battery costs:

Gartner developed their own hype cycle:

Hype Cycles and Priority Matrices offer a snapshot of the relative market promotion and perceived value of innovations. They highlight overhyped areas, estimate when innovations and trends will reach maturity, and provide actionable advice to help organizations decide when to adopt.

This is how it currently looks:

Diffusion of innovations - and especially the curve below is also often seen with regard to innovation:

Diffusion of innovations is a theory that seeks to explain how, why, and at what rate new ideas and technology spread. Everett Rogers, a professor of communication studies, popularized the theory in his book Diffusion of Innovations; the book was first published in 1962, and is now in its fifth edition (2003).[1] Rogers argues that diffusion is the process by which an innovation is communicated over time among the participants in a social system. The origins of the diffusion of innovations theory are varied and span multiple disciplines.

Rogers proposes that four main elements influence the spread of a new idea: the innovation itself, communication channels, time, and a social system. This process relies heavily on human capital. The innovation must be widely adopted in order to self-sustain. Within the rate of adoption, there is a point at which an innovation reaches critical mass.

The categories of adopters are innovators, early adopters, early majority, late majority, and laggards.[2] Diffusion manifests itself in different ways and is highly subject to the type of adopters and innovation-decision process. The criterion for the adopter categorization is innovativeness, defined as the degree to which an individual adopts a new idea.

Trying to understand these concepts as in investor (or just in general) - doesn’t mean you turn to high growth new type of technology companies. I feel it is just about having a broad understanding what might stay the same or what type of business models are under attack from new upcoming technologies.

Also - listen (recent ValueHive podcast) for example to Lawrence Hamtil - who talks basically the opposite of ARK namely business which he believes will remain the same the coming years (i.e. have a durable moat):

tobacco

railroads

defense

waste disposal

airports

specialty chemicals

Lots of these industries have a regulatory aspect that protects their moat.

And remember how Jef Bezos (Amazon) puts it:

“I very frequently get the question: 'What's going to change in the next 10 years?' And that is a very interesting question; it's a very common one. I almost never get the question: 'What's not going to change in the next 10 years?' And I submit to you that that second question is actually the more important of the two -- because you can build a business strategy around the things that are stable in time. ... [I]n our retail business, we know that customers want low prices, and I know that's going to be true 10 years from now. They want fast delivery; they want vast selection. It's impossible to imagine a future 10 years from now where a customer comes up and says, 'Jeff I love Amazon; I just wish the prices were a little higher,' [or] 'I love Amazon; I just wish you'd deliver a little more slowly.' Impossible. And so the effort we put into those things, spinning those things up, we know the energy we put into it today will still be paying off dividends for our customers 10 years from now. When you have something that you know is true, even over the long term, you can afford to put a lot of energy into it.”

Some things just keep on going - a bit like Jonathan - who is going viral on Twitter these days. Imagine being 189 years old. And we people still think we are the most fascinating creatures on this planet ;)

Today I came across this overview of the EV battery value chain. I always like these kind of industry (value chain) mappings. Also in discussions it provides a useful starting point / framework to see which players in the industry might capture a profitable part of the (ideally growing) pie.

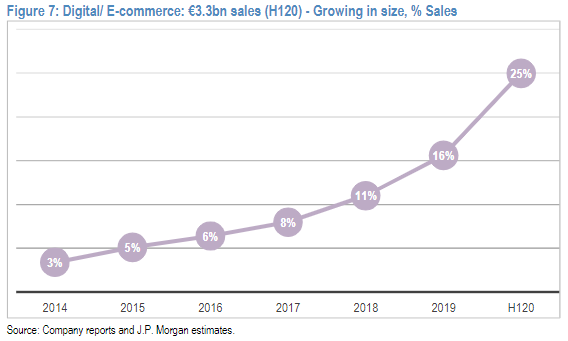

Some companies seemed to be particularly well prepared to deal with this pandemic. As in: their online operations where already up to speed and got an extra acceleration because of the pandemic situation. Companies on top of my mind are some high-quality consumer companies such as Nike and Estée Lauder. But also Starbucks for example which was/is rolling out the drive throughs. Another example was L’oréal reporting this week:

Thanks to its strength in digital and e-commerce, which has again increased considerably during the crisis, L’Oréal has been able to maintain a close relationship with all its consumers and compensate to a large extent for the closure of points of sale. As a result, sales achieved in e-commerce [5] rose sharply by +62% [1], across all Divisions and all regions, reaching the record level of 26.6% of the total Group’s sales for the year.

JPM did a nice analysis on the historical online exposure of L’oréal. A general snippet from their presentation (which can also be deducted from their public data):

There is also an extra dimension to it i.e. online advice - check out their website:

Really nice dive into Tencent - a fascinating company. Fundsmith also mentioned it in their yearly call: the two companies they are currently watching with interest are Tencent and TSMC.

It’s always better to get feedback from people who work in the industry.

Employees are of course a quality aspect of a company. But with a company like Texas Instruments - there is an extra aspect to it given there are only a few analog companies and it seems to be something that has to be learned on the job.

Enjoy!