2021:4 Druckenmiller buckle up, German companies can split-up, Estée Lauder, luxury marketing rules and short-selling

Snowy weekend in Belgium (which only means a few centimers of snow). Last week, equity markets recovered from their mini 5% end of January (deleveraging?) dip. Earnings season is in full swing with traditionally US companies reporting a bit earlier than European companies. And luckily - Gamestop is no headline news anymore.

Enjoy some snippets from what past by my home office desk this week!

Druckenmiller talked to GS: he is throwing in some “fun” interesting numbers:

buckle up - I have been doing this since 1978 - and this is about the wildest cocktail I have ever seen in terms of trying to figure out a roadmap

the 2020 recession was 5x the average recession since WOII but it did it in 25% of the time

11 mln. people were unemployed but we had the largest increase in personal income in 20 years because of policy response such as CARES Act - in 3 months we increased the deficit more than if you took the last 5 recessions combined (‘73 ‘75 ‘82 ‘90 ‘02 ‘08) and the FED bought more Treasuries in 6 weeks than they did in 10 years under Bernanke and Yellen

corporate borrowing went up USD 400 bn (versus down USD 500 bn during GFC)

since 2018 M2 in the US has grown 25% more than nominal GDP (25% increase in liquidity) versus in China M2 is where it was 3 years ago (they haven’t borrowed anything from their future)

value versus growth: higher inflation could make a more difficult set-up for growth but the comparisons with 2000 are ridiculous because we had a double whammy back then: overvaluation and the earnings were about to end (because lots of companies where about building the internet and that was already been done)

cloud: 4-5th inning - so long way to go

big tech underperformed recently (is GARP): seems like market has rotated in 40x sales or reopening plays

I like his down-to-earth response when the interviewer is trying to get an asset class / stock pick out of him: I own them all, I think more in a matrix, I don’t know what the market is going to do in the next week or two, no fan of traditional risk models…(but he does like Asia (China) it seems).

European industrials seem to enjoy their moment in the sun. The MSCI Europe Industrials is up 9% per annum the last 3 years (versus 5% broad market return).

Especially German engineering giant Siemens might have surprised some. The spin-offs did seem to create more focus and value for shareholders. From the FT:

Siemens boss Joe Kaeser has praised activist investors as he stepped down from the slimmed-down industrial group with its shares trading at all-time highs. His stance is unusual in Germany, where investors seeking to break up conglomerates were once pilloried as “locusts”. But Mr Kaeser said the prospect of activists demanding change at Siemens had acted as a catalyst for his own restructuring.

Shareholders say Mr Kaeser’s transformation of the 170-year-old company has done more than create an attractive asset for capital markets. It has proven that large, sclerotic German companies can be restructured. “Nobody else in Germany ever tried to do something like this,” said Ingo Speich, a portfolio manager at Deka, a top-10 Siemens investor. “It was high risk and it is a big achievement.”

The spin-off of Siemens Healthineers has led to a standalone company worth more than BMW, while the September flotation of Siemens’ energy unit is expected to further benefit the group.

By coincidence I saw this story with regard to GE:

Siemens and GE have each more than 200.000 people on their payroll - fair to say that is a lot an not easy to turn that kind of ship (or spin-off certain segments):

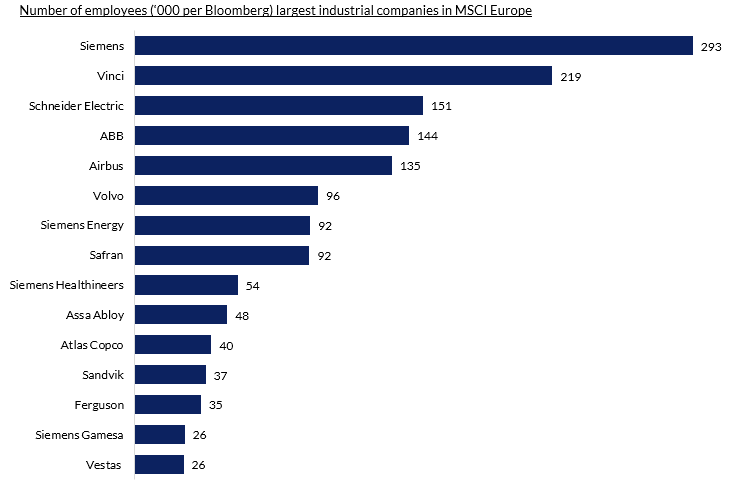

Out of curiosity I was looking at the number of employees of other companies, the median number of employees for companies in the MSCI Europe (about 450 biggest quoted companies) is about 22.000 (versus average 50.000). The bigger ones have business models that “require” a bigger workforce to operate (catering, food retail, security, car manufacturing, …). The other extremes are for example holdings and real estate (who are often run by only a few people):

German auto- and truckbuilder Daimler must have overheard something. They plan to split the industrial business into Mercedes-Benz (cars) and Daimler Truck (trucks):

Also Estée Lauder might have surprised some people (the market at least since it was up +7% on earnings) on the back of online sales and Asia:

In mainland China, net sales grew strong double digits, reflecting, in part, an outstanding performance related to the 11.11 Global Shopping Festival. The growth was led by skin care and fragrance, with the luxury brands outperforming. Sales increased double-digit in every channel, including both brick-and-mortar and online, with online representing more than half of total sales.

The Company plans to return to its long-term growth targets of 6% to 8% sales growth, 50 basis points of operating margin expansion and double-digit adjusted diluted earnings per share growth in constant currency after the recovery period from the pandemic.

Not a lot of companies/brands can put out these kind of metrics - especially knowing that about 20% is normally from travel retail.

And they might only getting started:

Interested in luxury (clothing, cars, alcohol,…) - be sure to check out the anti-laws of marketing from “The luxury strategy - break the rules of marketing to build luxury brands” (by Kapferer).

Especially the part around pricing and demand is key imo.

The closing remarks of Texas Instruments conference call from this and previous earnings call:

That concludes the call. So let me finish with a few comments on key items that we believe deeply. First, we run the company with the mindset of being a long-term owner. We believe that growth of free cash flow per share is the primary driver of long-term value. Our ambitions and values are integral to how we build TI stronger. When we're successful in achieving these ambitions, our employees, customers, communities and shareholders all win.

While we strive to achieve our objectives, we will continue to pursue our three ambitions: We will act like owners who will own the company for decades; we will adapt and succeed in a world that's ever changing; and we will be a company that we are personally proud to be a part of and would want as our neighbor. When we're successful, our employees, customers and communities and owners all benefit.

TI’s IR website (i.e. their capital allocation info) remains one of the best imo.

Gamestop is at least no daily headline anymore. Now come the long form analysis pieces. First of all with regard to the plumbing of the financial markets. I found this insightful (lots of other good ones floating around):

The FT also published some analysis - for a firm like Melvin to rebound - I guess it psychologically challenging to say the least:

Melvin is now faced with the task of picking itself up from the debacle, with the eyes of the industry upon it but at least with two powerful endorsements. “I’ve known Gabe Plotkin since 2006 and he is an exceptional investor and leader,” Cohen said last week as he doubled down on his protégé. Griffin, too, was public in his praise. “We have great confidence in Gabe and his team.”

I also listened to this - let’s say Cohodes doesn’t seem to be a huge fan of shops like Melvin. For Belgian readers: Cohodes is around for quite a while (from the WSJ in 2000):

The 40-year-old money manager, a general partner in the New York hedge fund Rocker Partners LP, was the most vocal short -- seller of stock in Lernout & Hauspie Speech Products NV, a Belgian speech-recognition software company. In August, on his Internet radio show, "The Other Side of the Tracks," Mr. Cohodes described L&H's revenue stream as "going from the left pocket to the right pocket." He accused the company's management of exaggerating its prospects, relying on rapid-fire acquisitions and reporting a dubious surge in Asian sales.

Enjoy!